March closes a quarter of equity rallies and a flat quarter for global fixed income. The reasons are the same as we have seen for the past few months.

- Optimism in view of lower interest rates

In November last year Jerome Powell, chairman of the FED (US central bank), said that there would be no more rate hikes and this triggered strong optimism, driving global stock indices to record highs. In fact, at the beginning of the year, investors were expecting up to 7 rate cuts by the Fed.

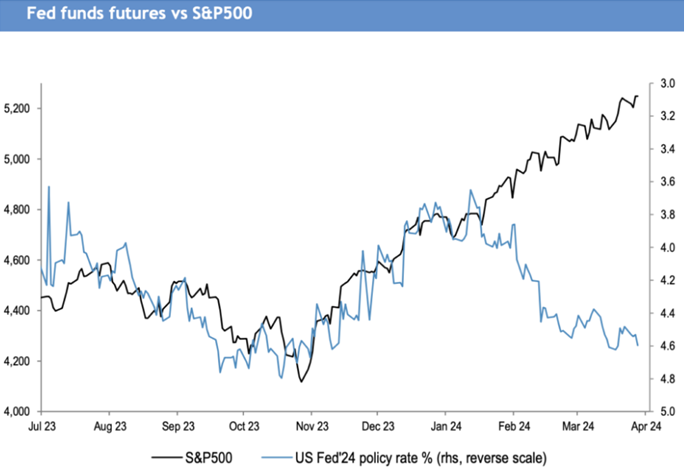

Today, after the economic recovery and the stubbornness of inflation to reach 2% has cooled the mood of the FED to lower rates. The market now expects 3 rate cuts instead of the 7 expected at the beginning of the year. Has this been reflected in market declines? Absolutely not. Take a look at this self-explanatory chart.

The light blue line is the interest rates whose scale is on the right (it is inverse, it goes from higher to lower to better understand the graph) and the dark blue line is the most representative index of the American market, the S&P500. A correlation is observed until the end of January 24 and then they deviate from each other. What the chart means is that, due to a drop in rates, the market reacts by going up (from November to January) but then rates go up and the market does not go down. Why? I think there are two fundamental reasons, i) liquidity in the system continues and ii) something the Anglo-Saxons call FOMO (Fear of Missing Out), i.e. fear of missing out on the rise.

That liquidity is still in the system can be seen in the balance sheet of the FED (one of the liquidity measures), before the pandemic it was at $4.2Tn (many zeros) and today it is at $7.5Tn (still many zeros but almost double). Liquidity is like water that spills over and looks for a place, liquidity looks for profitability, and if there are no real profitable investments, the quickest way is financial assets.

On the other hand, what is this FOMO? I remember that, in the Spanish real estate boom at the beginning of the century, there were people who saw how neighbors (sometimes brothers-in-law) sold their houses well above what they had bought them for and invested in others to sell them quickly, which generated an anxiety not to be left behind. The question is, could it be happening now, perhaps, we see it in the second reason below. It leads me to recall the figure of Daniel Kahneman, who recently passed away at the age of 90. Kahneman was a psychologist who won a Nobel Prize in economics for his work based on how both emotional and cognitive biases affect us when making decisions (I recommend reading “Think Fast, Think Slow”). He said “The illusion that we understand the past, fosters overconfidence in our ability to predict the future” and we follow what he calls the “herd effect”, in short, we see an upward market trend that does not let up, it makes us anxious and we buy without really understanding what is going on but it reassures me to know that others do.

2. Optimism of technological innovation under the new era of AI (Artificial Intelligence).

As in previous months, the market is rising thanks to companies linked in some way to AI. Will it go on rising forever, is it a bubble? I don’t know, but at least we should be cautious.

During the “.com” bubble at the turn of the century, companies were going up day by day. It seemed that the new paradigm, the Internet, meant that new technology companies would never go under, but something was wrong. The CEO of Sun Microsystems himself said that, if his company was trading at 10 times sales, it meant that, in order to return the money invested to shareholders, he had to wait 10 years of sales but assuming that he had neither costs nor expenses, in other words, an absurdity. Then the bubble burst, taking many technology companies with it.

Believe me, I don’t want to scare you, fortunately, we have a much better financial situation than that year but I think it is an important reference not to go crazy with what today is the new paradigm: AI. Of course, AI will change our lives as the Internet did more than 20 years ago. The problem is the valuation of many companies linked to AI.

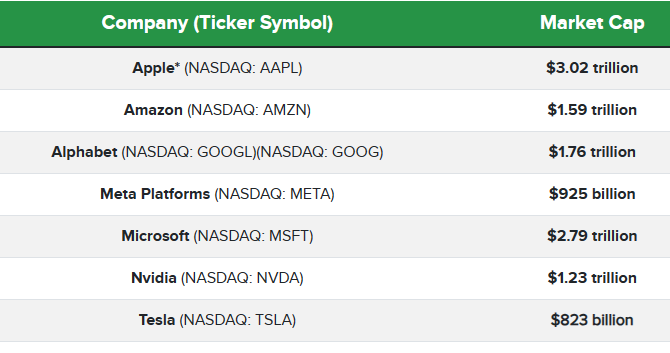

Look at this table of the market capitalization of the 7 companies that today they call the Magnificent 7 because they are the ones that are linked in some way to AI.

To put it in perspective, Spain’s GDP is $1.5Tn, below the top 5. To compare it with what the CEO of Sun Microsystems said, this is how these companies are quoted:

- Microsoft: 9.8 times sales

- Apple: 6.5 times

- Amazon: 1.9 times

- Google: 4.5 times

- Target: 4.7 times

- Nvidia: 22 times. EYE

- Tesla: 6.4 times

Therefore, beware that some of them are trading at somewhat demanding multiples.

By this I do not mean that there will be a recession that will take everything by storm, the economy is doing more or less well, the banks are healthier and there are high-quality companies outside of these 7 trading at lower multiples.

You can continue to invest but with prudence and if you do not understand where you are investing, you should take a step back and analyze the possible alternatives.

You can read the previous month’s market review here.